Gratuity Eligibility and Calculation: What HR Must Know

PAYROLL, PF & BENEFITS

Gratuity is a long-term statutory benefit that often receives attention only at the point of employee exit. For HR professionals, however, understanding gratuity eligibility, calculation, and compliance requirements is essential for accurate payroll planning and responsible employee communication.

This article explains gratuity in simple terms, focusing on when it becomes payable, how it is calculated, and what HR must manage proactively.

What Is Gratuity?

Gratuity is a statutory retirement benefit paid by employers to employees as a mark of service recognition. In India, gratuity is governed by the Payment of Gratuity Act, 1972.

It becomes payable when an employee leaves the organisation after completing a minimum period of service, subject to specific conditions.

Applicability of the Gratuity Act

The Act applies to:

Factories, mines, oilfields, plantations, ports, and railways

Shops and establishments employing 10 or more employees

Once applicable, the Act continues to apply even if employee strength later falls below ten.

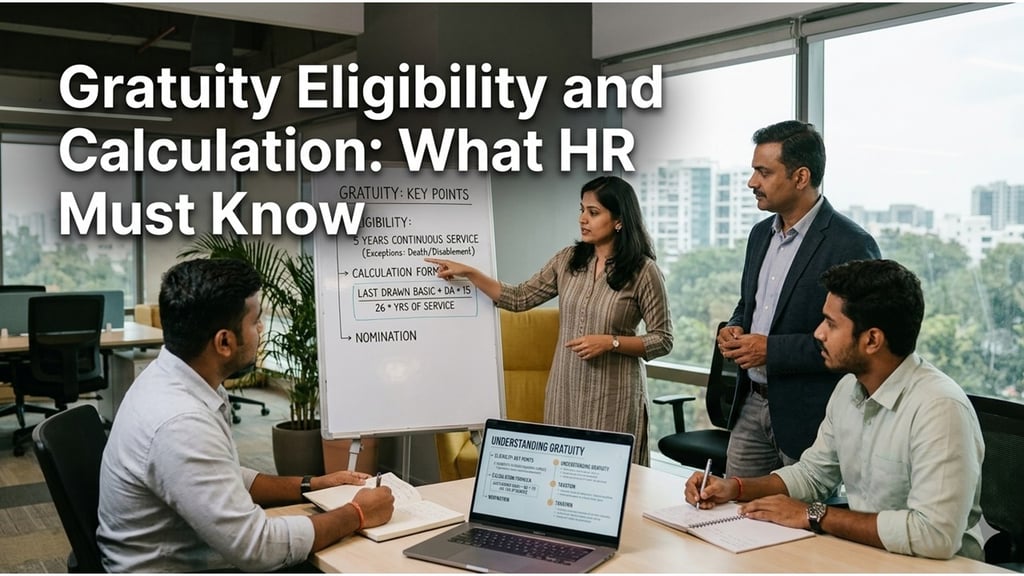

Eligibility for Gratuity

An employee becomes eligible for gratuity when:

They complete at least 5 years of continuous service, and

Their employment ends due to:

Resignation

Retirement or superannuation

Termination (other than misconduct)

Death or disablement (5-year rule does not apply)

Continuous service includes certain interruptions such as leave, sickness, and authorised absence.

How Gratuity Is Calculated

For employees covered under the Act, gratuity is calculated using the formula:

Gratuity = (Last drawn basic salary + DA) × 15 × Years of service ÷ 26

Key points HR should note:

Service beyond 6 months is rounded up to the next year

Maximum gratuity payable is subject to statutory limits

Gratuity is not paid monthly; it is a terminal benefit

Gratuity and Payroll: HR’s Ongoing Responsibility

Although gratuity is paid at exit, HR must:

Track employee service tenure accurately

Account for gratuity liability in payroll and finance planning

Ensure exit settlements include gratuity where applicable

Many organisations create gratuity provisions in their books even though payment is deferred.

Tax Treatment of Gratuity

Gratuity is tax-exempt up to prescribed limits under the Income Tax Act, subject to conditions. HR should:

Coordinate with payroll and finance teams

Provide accurate breakup in final settlement documents

Avoid giving informal tax advice without validation

Gratuity Management Checklist for HR

Use this checklist to manage gratuity responsibly:

Eligibility & Records

☐ Track date of joining accurately

☐ Monitor completion of 5-year service

☐ Maintain clean service records

Calculation & Payment

☐ Apply correct formula and rounding rules

☐ Verify last drawn basic and DA

☐ Include gratuity in full and final settlement

Compliance & Communication

☐ Inform employees about gratuity eligibility

☐ Respond to gratuity claims within timelines

☐ Retain gratuity-related documentation

Common Gratuity Mistakes HR Should Avoid

Assuming gratuity applies only at retirement

Missing eligibility due to incorrect service records

Confusing gratuity with PF or bonus

Ignoring gratuity liability in payroll planning

Gratuity compliance failures often surface only during disputes or audits.

Conclusion

Gratuity is a statutory obligation that reflects an organisation’s respect for employee service. When HR understands gratuity rules clearly and manages them consistently, exit processes become smoother and legally sound.

Conclusion--

Effective labour law compliance depends on how well HR operations, payroll, and business processes work together. When compliance is embedded into everyday workflows, organisations reduce risk, improve accuracy, and build sustainable governance systems. HR teams that prioritise integration over isolation are better positioned to manage compliance confidently and consistently.

Related Articles

HireDesk India © 2026 | All Rights Reserved

"Thoughtful guidance for everyday HR"

Quick Links

Topics

Connect

_______________________________________________________________________________________________________________________________________________________________________________________

HireDesk is a free HR knowledge platform focused on practical, India-specific workplace guidance. We help HR professionals, managers, and learners navigate people practices with clarity, responsibility, and real-world relevance.